The project’s founders actively disseminate claims regarding a client base exceeding 250,000, alongside endorsements via positive coverage across various financial news outlets. Assurances of zero-spread trading and nominal commission structures are prominently featured. Furthermore, marketing efforts highlight a diverse tier of trading accounts, enhanced leverage options, and round-the-clock customer support. Access to industry-standard software, including MetaTrader 5, is also purported. In this Skyriss review, we will scrutinize whether the venture warrants institutional trust or if it exhibits the hallmark characteristics of a fraudulent operation.

Contents

- Key Points to Know

- What Stands Out About the Skyriss.com Website?

- Inside the Offshore Registration of Skyriss

- Trading Conditions Explained

- Checking Compliance with Legitimate Rules

- How Long Has Skyriss Really Been Around?

- Platform and Support Overview

- Online Reputation: What We Found

- Conclusion: Risks and Reliability of Skyriss

- Sources

Key Points to Know

| Main Website | https://www.skyriss.com |

| Additional Domains | https://crm.skyriss.com/register |

| Online Since | 28/11/2024 |

| Legal Entity Name | Skyriss Securities Ltd |

| Pretended to Be Regulated | MFSC |

| Fact-Checked Regulation | MFSC |

| Deposit to Start Trade | $10 |

| Leverage up To | 1:500 |

| Spreads From | 0.0 pips |

What Stands Out About the Skyriss.com Website?

[review]

Inside the Offshore Registration of Skyriss

The firm operates not merely under offshore supervision but is also legally domiciled within an offshore jurisdiction, specifically holding registration in Mauritius. While incorporation in Mauritius does not automatically serve as a definitive red flag, it is fundamentally distinct from robust, mainstream regulatory compliance.

Operating under the aegis of such a jurisdiction introduces profound vulnerabilities for the dealer. The reasons are as follows:

- Professional market participants routinely eschew brokers lacking oversight from Tier-1 regulators; this cautious approach extends directly to corporate registration.

- Securing cost-effective and dependable merchant acquiring services is notoriously difficult for such entities. Consequently, firms of this nature are frequently compelled to rely on crypto-asset rails or convoluted payment workarounds.

- Offshore brokers encounter friction, if not outright barriers, when attempting to interface with Tier-1 liquidity providers, who generally decline engagements with offshore entities.

- These operations face stringent promotional prohibitions, regional operational restrictions, and persistent regulatory domain blocks.

Thus, a granular analysis of skyriss.com underscores the reality that offshore corporate registration remains a significant structural deficit and a warning sign for discerning investors.

Trading Conditions Explained

The broker architecture deploys several trading account tiers, spanning from Raw to Institutional. Variations between these tiers are dictated by minimum capital requirements and supplementary services. Below, we dissect the available financial instruments, minimum deposit thresholds, and leverage ratios, alongside an examination of spreads, commissions, and ancillary services.

So, the brokerage platform offers engagement across multiple asset classes, including currency pairs, commodities, indices, stocks, ETFs, and cryptocurrencies. However, specific details regarding the exact depth of the asset catalog remain undisclosed, while the proprietary constraints of the provided terminal further restrict market access.

While entry-level access is pegged at a modest $10, premium accounts demand commitments of $1,000 and $10,000 respectively. The administration effectively monetizes preferential trading conditions. The capital attraction strategy here is elemental: entice a high volume of retail participants by leveraging low-barrier deposit narratives — a tactic overwhelmingly prevalent among illicit brokers and loosely regulated offshore operations.

The leverage structures extended by the broker are remarkably aggressive, climbing to ratios as high as 1:500. Though permissible under lax offshore frameworks, such exposure is far from an advantage. When combined with the inherent volatility of CFDs, the probability of immediate capital depletion is exceptionally high, exposing novice traders to acute risk.

The platform similarly promotes an array of value-added services, including e-books, video modules, instructional guides, market commentary, and analytical forecasts. The firm also advertises affiliate frameworks, including PAMM, MAM, and Introducing Broker (IB) models. Yet, the total absence of verifiable operational details surrounding these programs serves as another indicator of non-compliance.

Checking Compliance with Legitimate Rules

The legitimacy of Skyriss represents a critical focal point, as offshore regulatory assertions invariably demand rigorous independent validation. To that end, we decided to investigate the firm’s physical footprint, corporate transparency, and the feasibility of fund recovery via professional legal channels.

Skyriss claims licensure by the Financial Services Commission of Mauritius (FSC). While a cross-reference with the official MFSC registry does confirm the existence of a certificate, such oversight offers virtually no consumer protection. Consequently, friction regarding withdrawals is highly probable, as is the risk of arbitrary account suspension or chart manipulation via a highly controlled, substandard trading terminal.

The corporate address listed by Skyriss confirms an offshore domicile in Mauritius. However, verification via geospatial mapping tools fails to corroborate any physical corporate presence, a discrepancy typical of shell companies. Transparency is further compromised by the absolute anonymity surrounding the firm’s executive leadership — a definitive red flag in contemporary financial services.

How Long Has Skyriss Really Been Around?

The operational longevity of a market intermediary is easily unmasked via WHOIS and WebArchive databases. Records indicate that while the underlying corporate entity was established in 2024, a substantive operational footprint and licensing only emerged in 2025. Thus, the broker is a very recent market entrant. When viewed alongside its negligible digital footprint and lack of brand equity, this brief tenure must be interpreted as a severe vulnerability.

Platform and Support Overview

The digital storefront utilizes a standardized white-label iteration of MetaTrader 5. Although MT5 is a legitimate platform adopted by reputable brokers, in this specific operational context, it presents severe risks. The software is entirely subject to internal administrative privileges, granting managers direct control over execution speeds, commission overrides, and spread adjustments. At the time of writing, this architecture appears optimized to gradually erode client balances.

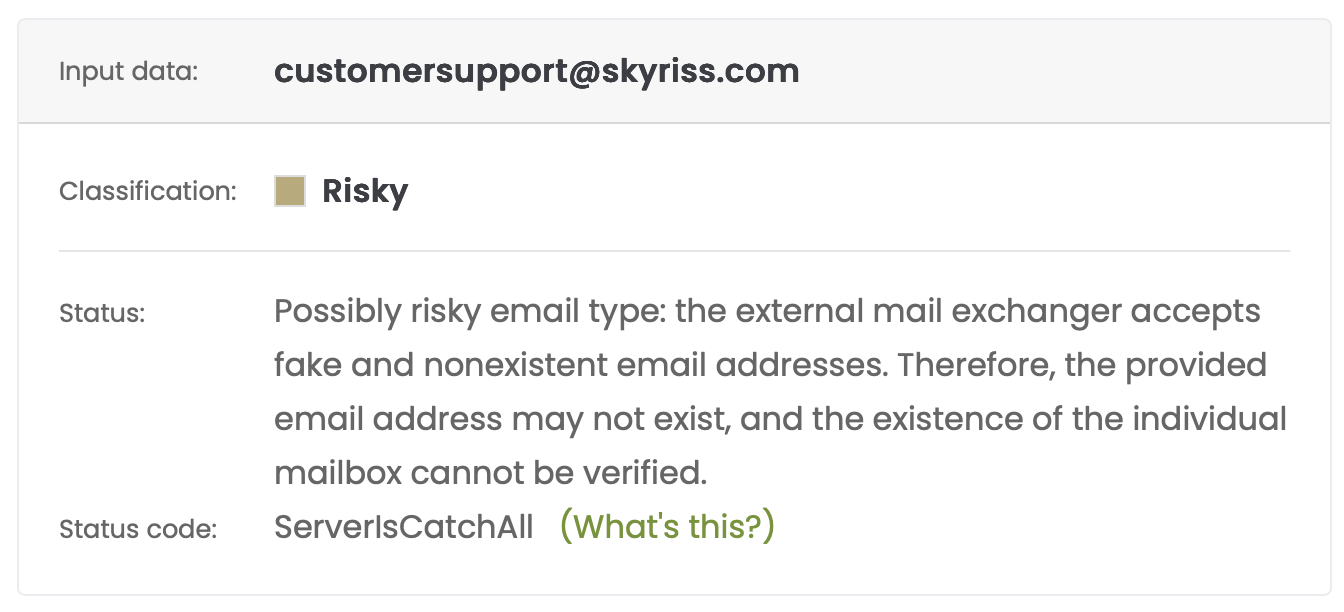

Customer communications are routed via a solitary email address. Technical validation of this email domain suggests that interacting with the support infrastructure poses data security risks, with a high probability of personal data exposure. Furthermore, the website lacks a live-chat feature, relying instead on a single external messaging application. While links to corporate social profiles exist, engagement is virtually non-existent.

Online Reputation: What We Found

Skyriss suffers from a distinct lack of market recognition. Within established trading communities and on reputable review aggregators, the sentiment is overwhelmingly critical, punctuated by sparse, overtly fabricated positive commentary.

Conclusion: Risks and Reliability of Skyriss

In light of the evidence, we have decided to explicitly advise against any engagement with this broker. The project operates under a compromised offshore framework, generates significant client hostility, utilizes a highly manipulated trading environment, and maintains an uninformative, opaque digital interface.

Sources

- WHOIS domain registration data.

- Financial Services Commission (Mauritius) Registry.

- Email domain authentication and security validation.

- Company profile with a warning on Trustpilot.

- Skyriss feedback on WikiFX.

26.05.2026 at 10:13

So-so

Skyriss appears to be a powerful platform and even has a Mauritian license, which is generally acceptable for online brokers. However, I would be wary of investing large sums of money here. I see that they have enough money to market themselves on financial portals, but an audience is earned through years of work and satisfied traders. It’s still too young to be completely trusted and there’s no guarantee that one day we won’t see a notice on those same financial portals that the Mauritian commission has fined them or revoked their license, as often happens. So time will tell…