The administration of the intermediary actively promotes a range of ancillary services. Particular attention is given to access to various trading accounts with differentiated features. The project is licensed by an offshore commission and holds legal registration with the same authority. Managers further highlight the implementation of assorted innovations, notifying clients through a dedicated section of the website. Despite this promotional effort, offshore licensing does not equate to reliability. A clear orientation towards contracts for difference remains a conspicuous warning sign. In this CapPlace review, we decided to examine whether the platform bears the hallmarks of a fraudulent operation.

Contents

- Key Points to Know

- What Stands Out About the Capplace.com Website?

- Inside the Offshore Registration of CapPlace

- Trading Conditions Explained

- Checking Compliance with Legitimate Rules

- How Long Has CapPlace Really Been Around?

- Platform and Support Overview

- Online Reputation: What We Found

- Conclusion: Risks and Reliability of CapPlace

- Sources

Key Points to Know

| Main Website | https://www.capplace.com/ |

| Additional Domains | Not Found |

| Online Since | 2024 |

| Legal Entity Name | Robertson Finance Inc |

| Pretended to Be Regulated | MISA |

| Fact-Checked Regulation | MISA |

| Deposit to Start Trade | $250 |

| Leverage up To | 1:200 |

| Spreads From | Undisclosed |

What Stands Out About the Capplace.com Website?

-

Details of the brand’s legal registration are disclosed.

-

Licensing by a questionable offshore commission.

-

Negative client feedback and allegations of fraud.

-

Extremely high leverage.

-

Reliance on contracts for difference.

-

A controlled trading terminal.

Inside the Offshore Registration of CapPlace

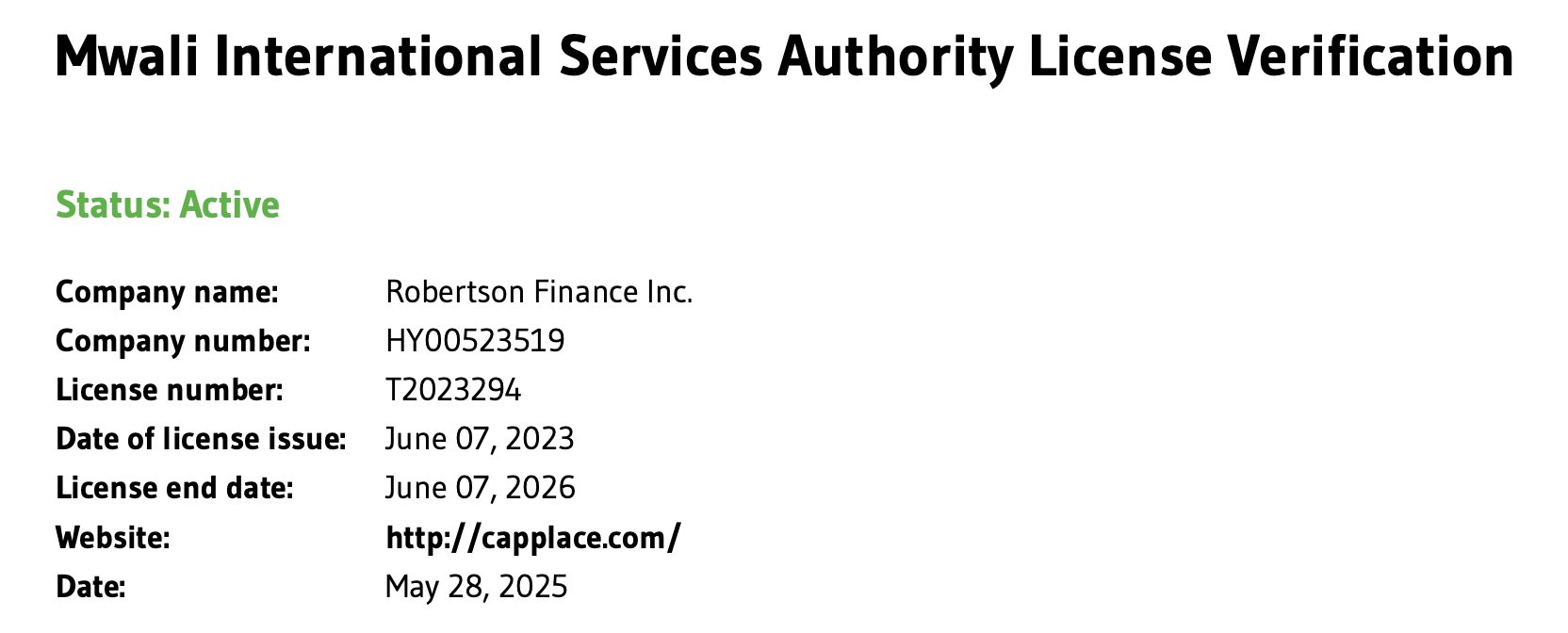

The intermediary is legally registered offshore. A license issued by Mwali International Services Authority (MISA) simultaneously signifies regulation and incorporation within the relevant jurisdiction. On the surface, this may appear to be a partial advantage: the firm is not entirely anonymous.

Offshore registration remains a direct indicator of elevated risk. Funds transferred to the company are credited to an offshore entity’s account. Any subsequent dispute requiring legal intervention may demand substantial financial resources, often exceeding the client’s initial losses. We wonder how many retail traders realistically possess the means to pursue such cross-border claims.

Trading Conditions Explained

In this capplace.com review, we consider the core trading conditions offered by the broker. The platform provides several account tiers, including Silver, Gold, and Platinum. The principal distinction between them lies in the scale of spread discounts. We decided to explore the available financial instruments, the minimum deposit, leverage, commissions, spreads, and additional services.

CapPlace grants access to currency pairs, commodities, and cryptocurrencies. However, the precise number of instruments is not disclosed. Within the browser-based terminal, the selection may be even narrower. The platform’s focus on contracts for difference is unmistakable. This segment is inherently high-risk and materially shapes the partnership between broker and client.

Notably, the official website provides no explicit risk warning regarding CFD trading. Established and properly supervised brokers are typically obliged by reputable regulators to publish precise statistics on the proportion of losing retail accounts and to update such data quarterly. No such transparency is present here.

The minimum deposit stands at $250. This information is disclosed only within the FAQ section and is absent from the account comparison table. While such practice is not unusual, it offers no assurance of safety. Even a 250-dollar transfer may be precarious in light of offshore oversight and other structural concerns. In certain cases, the administration may require larger sums for premium accounts in exchange for nominal privileges.

Leverage is fixed at 1:200. Although offshore regulators permit such levels, the impact on trading outcomes is significant. Clients face a heightened probability of rapid losses, potentially within their initial transactions. The combination of high leverage and CFDs amplifies exposure. We tend to regard this leverage level as a substantial red flag, particularly as it applies uniformly across all account types.

Additional services receive limited attention. Educational materials are confined to a basic FAQ section. There is no access to structured learning resources, webinars or thematic literature. Other privileges remain undefined, suggesting that expectations of high-quality support may be misplaced.

Checking Compliance with Legitimate Rules

The regulatory status of CapPlace is of decisive importance, as it directly shapes the trading environment and the level of protection afforded to clients. We will examine the project’s licensing framework in greater depth, consider the transparency of its declared headquarters, assess the degree of administrative secrecy, and address the realistic prospects of fund recovery with professional legal assistance.

CapPlace operates under a license issued by the offshore regulator Mwali International Services Authority (MISA). This can be verified either through the link provided on the broker’s official website or by independently consulting the regulator’s public register. However, the mere existence of such a license can scarcely be regarded as a substantive advantage. Offshore supervisory bodies are widely criticized for exercising only limited oversight over licensed brokers. In practice, they frequently demonstrate a lack of engagement with traders’ complaints and prove ineffective in resolving disputes.

Moreover, cooperation with an offshore-regulated intermediary carries persistent structural risks. Clients may encounter refusals when attempting to withdraw funds, unexpected account suspensions, or questionable adjustments within the trading terminal itself. We wonder whether retail investors fully appreciate how restricted their legal recourse may become once capital is transferred to an offshore entity.

Established and properly supervised brokers typically publish both their registered office address and the location of their operational headquarters. CapPlace does not. The contact section contains only a telephone number and an email address; no physical office address is disclosed. Equally concerning is the absence of information regarding the company’s executive leadership. Such opacity is not incidental. It is a policy frequently associated with organizations seeking to shield decision-makers from accountability.

How Long Has CapPlace Really Been Around?

The broker’s website features a section devoted to its corporate history. However, the information presented is superficial and devoid of measurable milestones, operational statistics, or verifiable achievements.

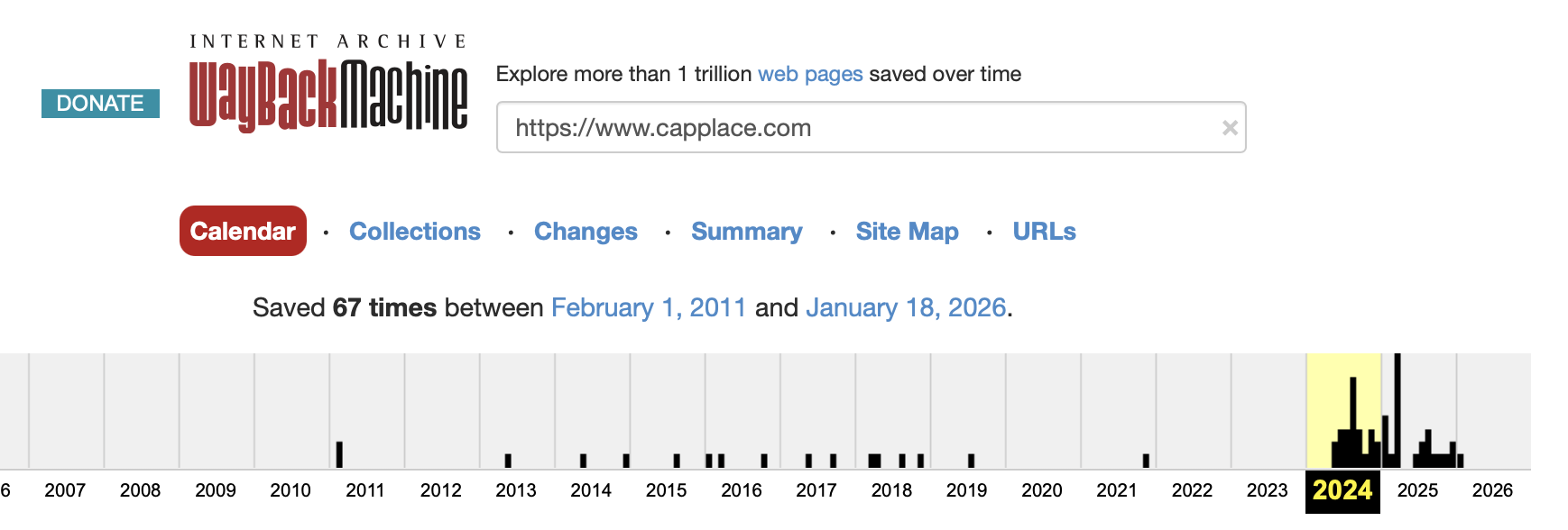

A WHOIS domain check yields little substantive detail. By contrast, archival data from WebArchive indicate that the intermediary has been active only since 2024. This timeline corresponds with the firm’s minimal market visibility and the limited volume of publicly available reviews. We believe that such a brief operational history does little to inspire confidence, particularly in a sector where longevity and reputation remain critical indicators of stability.

Platform and Support Overview

Clients of CapPlace are provided with rudimentary trading software. The CapPlace trading platform is a restricted WebTrader terminal with limited functionality. Such browser-based systems are frequently employed by questionable operators and are often cited by former clients as mechanisms through which balances gradually diminish.

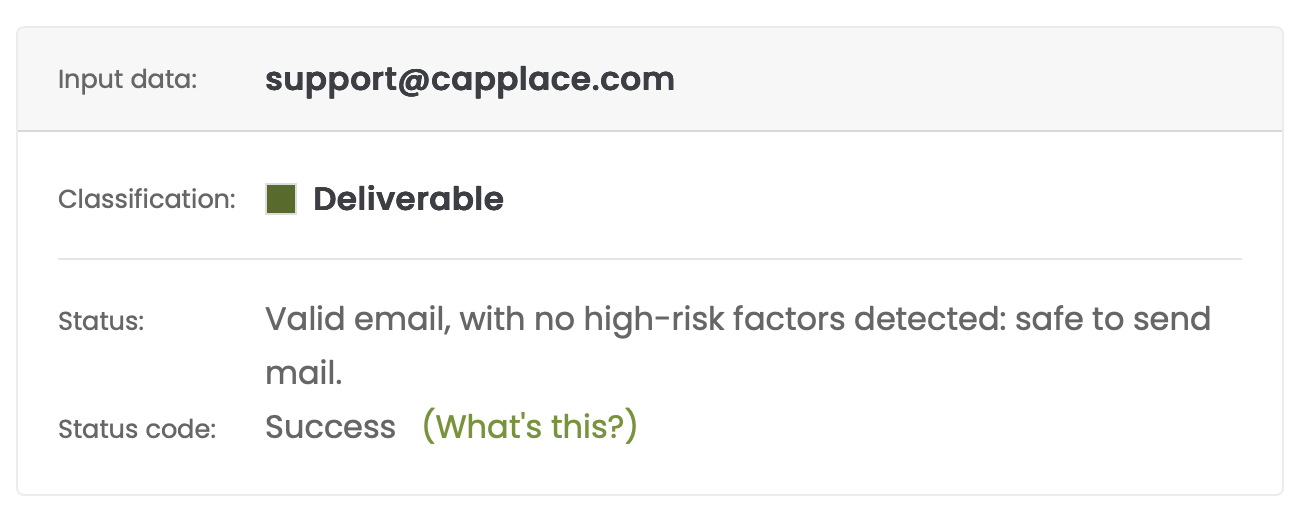

Customer service is available via email and mobile telephone. Email validation confirms that the address provided is technically active. However, technical validity does not equate to professionalism or efficiency. The operating hours of the support team are not specified. Furthermore, the absence of official social media accounts suggests an almost negligible public presence. We wonder why a company purporting to serve an international clientele would refrain from maintaining transparent communication channels.

Online Reputation: What We Found

A review of major trust-based platforms reveals a predominance of negative commentary concerning CapPlace. The overall trust rating hovers at approximately one out of five. The majority of reviews refer to withdrawal difficulties, alleged fraudulent conduct, and other contentious practices. Clients express marked dissatisfaction with their experience.

It is worth noting that the administration has responded to certain public complaints. These responses, however, are formulaic in tone and lack substantive engagement with the specific issues raised. Rather than providing clarification or evidence, they tend to rely on generalized statements.

Conclusion: Risks and Reliability of CapPlace

We advise against entering into cooperation with CapPlace. The firm operates under a questionable offshore regulator, attracts negative feedback, and faces allegations of misconduct. The use of a controlled terminal and a pronounced reliance on contracts for difference further intensify concerns.

Sources

- Domain history review via WebArchive.

- Verification of the regulatory license.

- Validation of the broker’s email address.

19.02.2026 at 17:09

It's a pity that I opened an account

I would strongly advise against even attempting to cooperate with this company. The dealer is an ordinary scammer hiding behind an offshore license. I personally lost around 2,000 dollars while dealing with them. Is this a sufficient price for foolishness??

08.03.2026 at 01:51

All comes down to blocking

Appalling quality of Capplace support The staff are rude and incapable of resolving issues. In the end, I was unable to recover my blocked account. They said that it was solely my fault since I violated certain rules and the account was blocked in accordance with the regulations I accepted. But when I challenged their opinion with evidence, they simply stopped responding and that was it…